Summary of Project Results

When studying the allocation of household assets, virtually all existing papers start with the household as the primitive unit of analysis (Gomes et al. 2020). In most models, a household is an imagined individual solving the optimal portfolio problem with a well-defined set of goals and constraints. In the empirical analysis, it is common to treat a household as an average of all its members or to use the head of the household to represent the entire household, without further considering how each household member may play a different role or have a different say. These treatments, by simplifying the portfolio-choice problem, allow researchers to focus on other important aspects of household finance. However, they embed a fundamental disconnect between individuals and households: household members may have different characteristics and need to resolve their differences to make financial decisions for the household.

Risk preference, for example, is a key determinant of portfolio choice under standard portfolio theory, and it has been observed that members of the same household often report different attitudes toward risk. When such internal disagreement occurs, household members will inevitably need to bargain with each other in order to make decisions for the entire household. What characteristics determine an individual's bargaining power when making financial decisions? Which characteristics are quantitatively more important? Between men and women, is there a gender gap in bargaining power? If so, what drives it?

Existing approaches

A budding literature begins to tackle these questions with two main approaches. The first approach links the variation in individual-level characteristics to household-level outcomes (e.g., Addoum 2017; Olafsson and Thornqvist 2018; Ke 2020). This approach can establish the relevance of a plausible factor, but is restricted by the availability of plausible instruments. Therefore, it usually does not allow for a quantitative comparison among multiple factors. A second approach finds an empirical proxy for bargaining power and studies its properties and determinants (e.g., Friedberg and Webb 2006; Yilmazer and Lich 2015; Zaccaria and Guiso 2020). A popular proxy is constructed based on so-called “final say” question, whereby each household is asked to report who has ultimate responsibility for making a decision in financial matters and acts as the “financial head” of the household. However, when separately surveyed, different household members often give different answers to the same question, suggesting nontrivial noise and disagreement. Furthermore, a common concern about survey responses directly used in this survey-based approach still lingers: is what people say consistent with what they do?

Our approach

We propose a novel approach that directly estimates bargaining power by combining individual risk preference with household portfolio choice. The basic intuition is that household members with more bargaining power are more able to incorporate their own risk preferences into the household's overall portfolio decision. This departs from the survey-based approach by examining what people actually do rather than what they say. By explicitly modeling the portfolio-decision process and the determinants of bargaining power, we also depart from earlier approaches by studying multiple channels—such as income, employment status, education, and personality traits—at the same time and quantifying each channel's relative importance.

With this idea in mind, we build a tractable model of intra-household financial decisions and structurally estimate it using detailed longitudinal data. In our model, spouses differ in their risk preferences and other individual characteristics, and they make portfolio decisions for the entire household portfolio in two steps. In the first step, they cooperatively decide on a household risk preference, which is the weighted average of their respective risk preferences. The weight represents each individual's bargaining power and is determined by spousal differences in individual characteristics and a gender effect. In the second step, the household makes portfolio decisions based on this household-level risk aversion as if it were a single individual, with additional considerations, such as wealth, participation cost, family size, literacy, and education, as suggested in the literature. The household then decides whether to participate in the stock market (the extensive margin) and by how much (the intensive margin), in the spirit of the Merton model. We estimate the model using panel datasets from three countries: Australia, Germany and US. We adopt the maximum likelihood method in the estimation, with stock market participation and risky asset holdings as the two outcome variables.

Results 1: Men have more bargaining power in financial decisions

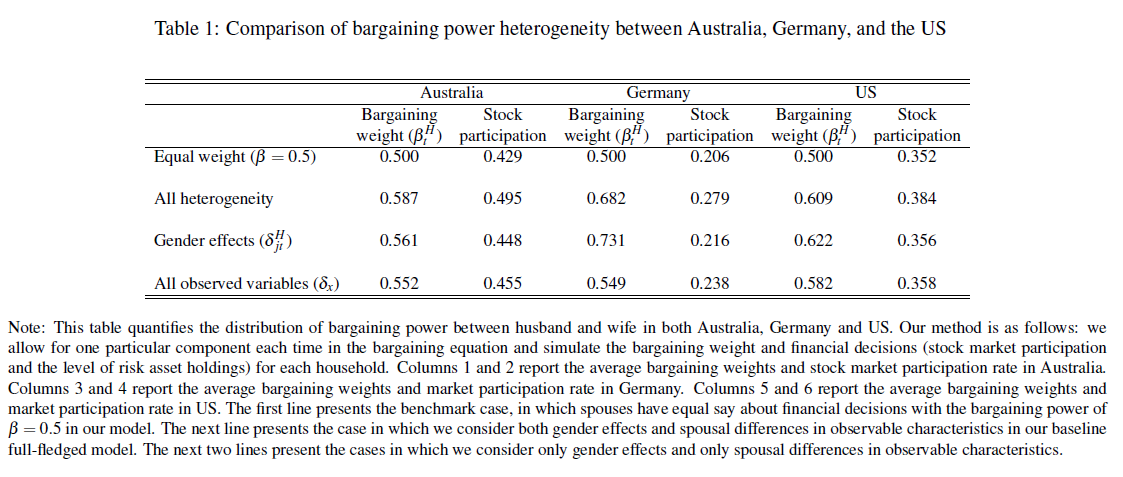

We estimate our model using panel samples from three different countries: Australia, Germany and US. Our estimation result shows a significant gender gap in the bargaining power: in the average Australian household, the weight placed on husband's risk preference is about 0.587, while the weight placed on the wife's is 0.413; in the average German household, the weight placed on husband's risk preference is about 0.682; and in the average US household, the weight placed on husband's risk preference is about 0.609. (see table 1) Consistent with a greater gender gap among the German population, German households show a much more traditional attitude toward gender roles according to the World Values Survey (Ke 2018).

Result 2: The gender gap in bargaining power can be traced back to observed characteristics as well as a gender effect

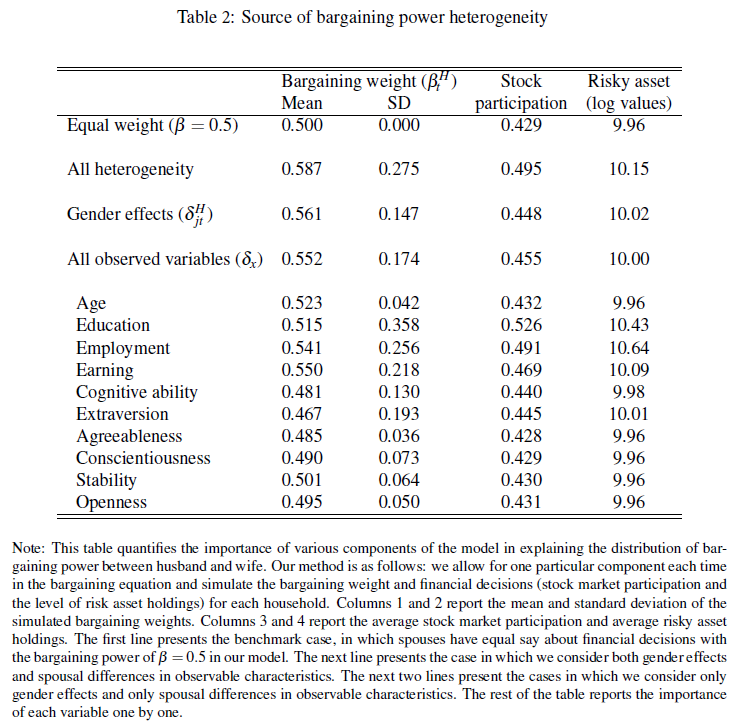

Our subsequent analysis tries to understand the sources of the gender gap in bargaining power. While the gap is partially explained by gender differences in individual characteristics such as income and employment, it is also due to gender effects. Overall, income, employment, and age tilt bargaining power toward the husband, as men on average earn more, are more likely to be employed, and are older. However, all observable characteristics combined can only account for above half of the gap, leaving the other half unexplained. This suggests a gender effect that contributes to husbands' disproportionally high bargaining power. (see table 2)

Result 3: The gender effect is associated with gender norms

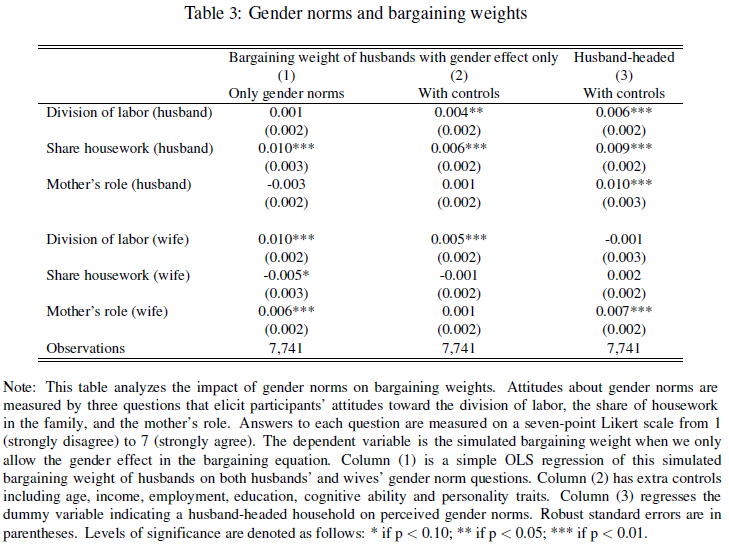

We link the gender effect to direct measures of gender norms. The Australian Survey includes three specific questions about gender norms, and husbands and wives need to answer these questions separately. The questions elicit attitudes toward traditional gender roles and how housework and childcare studies should be shared. We find that households with progressive attitudes toward gender norms are more likely to elect the wife as the head of the household, thereby empowering women with more say in financial decisions. In particular, we find those subjective perceptions of both the husband and the wife matter (see table 3).

References

Addoum, J. M. (2017). Household portfolio choice and retirement. Review of Economics and Statistics, 99(5):870–883.

Friedberg, L. and Webb, A. (2006). Determinants and consequences of bargaining power in households. Technical report, National Bureau of Economic Research.

Gomes, F., Haliassos, M., and Ramadorai, T. (2020). Household finance. Journal of Economic Literature, forthcoming.

Ke, D. (2018). Cross-country differences in household stock market participation: The role of gender norms. In AEA Papers and Proceedings, volume 108, pages 159–62.

Ke, D. (2020). Who wears the pants? gender identity norms and intra-household financial decision making. Forthcoming at Journal of Finance.

Olafsson, A. and Thornqvist, T. (2018). Bargaining over risk: The impact of decision power on household portfolios.

Yilmazer, T. and Lich, S. (2015). Portfolio choice and risk attitudes: a household bargaining approach. Review of Economics of the Household, 13(2):219–241.

Zaccaria, L. and Guiso, L. (2020). From patriarchy to partnership: Gender equality and household finance. Available at SSRN 3652376.

Impact and outputs

As suggested by Keynes fund, we have submitted a working paper version of the research output to the Cambridge Working Papers in Economics. https://www.econ.cam.ac.uk/research/cwpe-abstracts?cwpe=2130. The same working paper is also disseminated through multiple networks, including IFS working paper, https://ifs.org.uk/publications/15437, as well as SSRN working paper, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3814200.

We also presented this paper in many seminars to collect some useful comments, including Cambridge, Essex, Edinburgh, UC Irvine, IFS WiP Seminar. This work has also been presented in various conferences, including MFA, , EEA-ESEM Congress, EFA, IZA/SOLE Transatlantic Meeting for Labor Economists, Paris December Meeting

Future plans

In the coming weeks we will submit the current working paper to a world-leading top finance journal (such as Review of Finance Studies or Journal of Finance) to seek for a publication there. Furthermore, we plan to further extend our model in two dimensions: 1. We would like to extend our static model to a dynamic set-up. 2. We would like to incorporate intra-household bargaining over beliefs or other types of preferences. We expect that this follow-up research, which is likely to have substantial policy impact, will continue for the next few years.